Market Sentiment

Primary Assets Affected

Table of Contents

- The biggest listing the U.S. market has ever seen

- What actually happened on day one

- The market mechanics: from IPO price to $2.2 trillion

- The Musk premium, on the tape and in the chain

- The leveraged ETF wave: 25 funds already live

- Retail math and the small-investor squeeze

- What changed underneath: the AI optionality

- What NQ traders watch Monday

- Risks and what we do not know

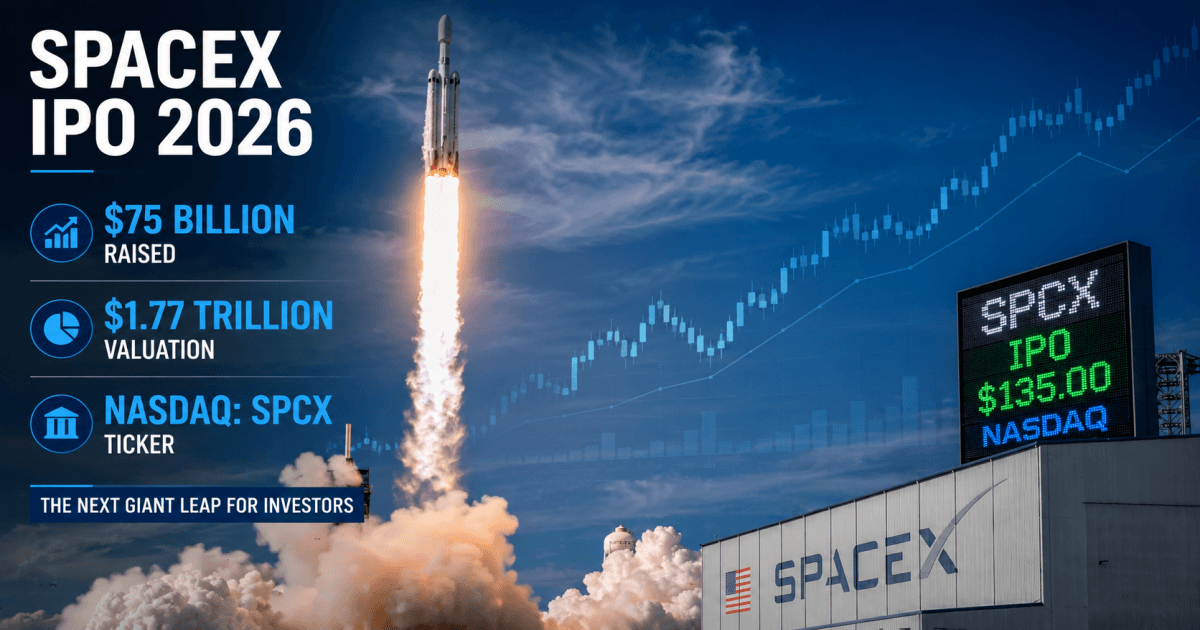

The biggest listing the U.S. market has ever seen

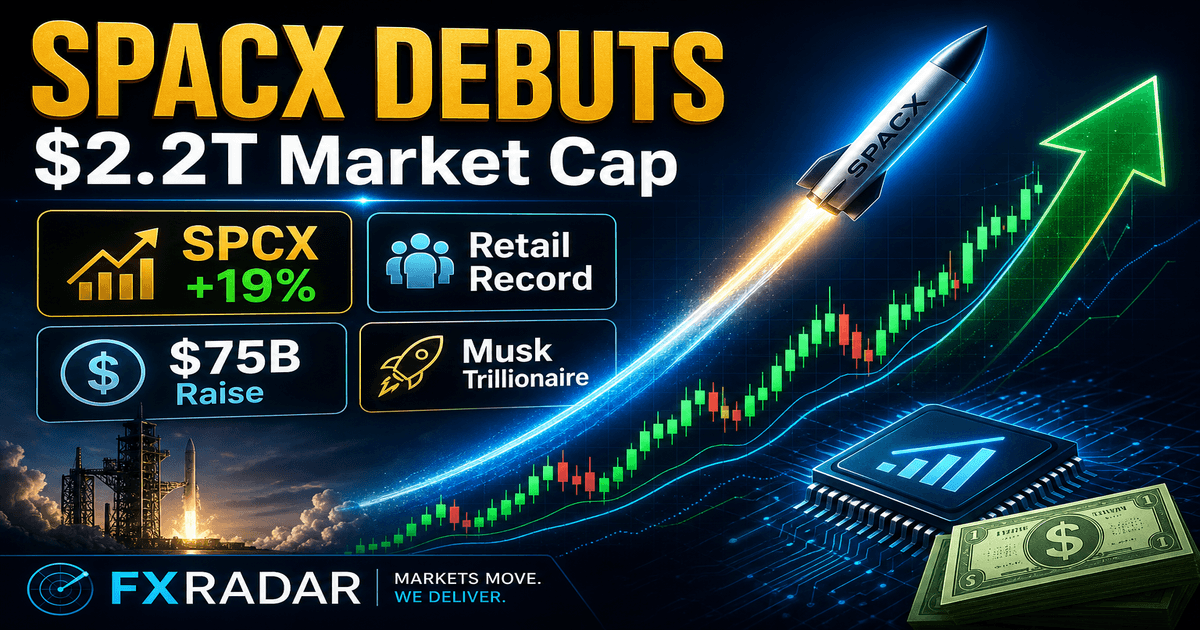

Space Exploration Technologies, the Elon Musk-controlled rocket and satellite group, made its Nasdaq debut on June 12, 2026 and closed the day as the sixth most valuable company in the United States. The deal raised $75 billion by selling 555 million shares at $135, the largest IPO in world history, before the stock ran to a session high of $176.52 and finished regular trading at $160.95, a 19% pop on day one. In the after-hours session, shares tacked on another 3.5% to $166.76, lifting implied market cap toward $2.2 trillion and putting SpaceX within striking distance of Amazon's roughly $2.54 trillion valuation.

For Nasdaq traders, the question is no longer whether the deal priced. The question is what week two looks like, and whether the launch pad holds once retail euphoria meets institutional profit-taking, index inclusions and a wave of leveraged ETFs that are already registered to trade.

What actually happened on day one

CNBC's live coverage captured the unusual mechanics of the listing. The opening trade came together faster than Nasdaq's own team expected, with Morgan Stanley leading the stabilization process and the first print landing at $150 on 58 million shares. Volume for the day topped 500 million shares, more than ten times what the second-largest IPO of the year, Cerebras, managed on its own debut. SpaceX alone traded more dollar volume than both the QQQ and SPY ETFs combined on Friday, with cumulative turnover just under $33 billion.

Citadel Securities, the largest retail wholesaler on U.S. exchanges, said SpaceX drew the highest IPO auction order activity on record from individual investors. VandaTrack data showed SpaceX as the most-bought single stock on Friday, with net retail buying running at more than three and a half times the level of second-placed Nvidia. Retail turnover hit $453 million, or about 4% of all single-stock retail activity on the day, putting the listing on track to surpass Coinbase's first-day retail record from April 2021.

The scale created operational strain. Robinhood reported record traffic and intermittent latency on its platform as users tried to add SPCX. Some retail investors who requested 1,000 shares through Robinhood received allocations of just 17, a frustration echoed across Reddit and other retail forums. By the close, even skeptics on Wall Street were watching the tape.

The market mechanics: from IPO price to $2.2 trillion

At its session high, SpaceX briefly traded with a market capitalization of about $2.21 trillion. The stock opened 11% above its $135 IPO price, then pushed another 14 points higher through the day as institutional desks covered short positions and momentum traders chased the move. By the closing bell at 4 p.m. ET, the listing had joined a very small club: U.S. companies worth more than $1 trillion. It did so on day one.

The numbers raise an obvious question. SpaceX generated $18.7 billion in revenue last year and lost $4.9 billion. That is a fraction the size of the next-smallest trillion-dollar member by sales, Micron, and a stark contrast to the profitability of the rest of the trillion-dollar club. CFRA analyst Keith Snyder assigned the stock a sell rating with a 12-month price target of $115 on Friday, well below the IPO price, telling CNBC the growth assumptions required to justify a $1.77 trillion valuation are "borderline comical." Other voices on the desk were less skeptical. Altimeter Capital's Brad Gerstner, who participated in the offering, framed SpaceX as a long-duration AI infrastructure play and called the current price "appropriate today" with multi-year upside if the data-center business executes.

Source: NASA / Tony Gray and Tim Powers, public domain, via Wikimedia Commons.

The Musk premium, on the tape and in the chain

Friday's trading created a handful of immediate second-order effects that NQ traders should be tracking into Monday's open.

Source: CNBC / Photo by Adam Jeffery, via CNBC live coverage.

Tesla (TSLA) gave back about 2% on Friday as attention and capital rotated into the new listing. Tesla's roughly $1.2 trillion market cap is now smaller than SpaceX's, a reversal of the historical pecking order between Musk's two public companies. An amended IPO filing disclosed that SpaceX may issue "significant equity" to fund future transactions, fueling fresh speculation about a Tesla-SpaceX combination or a broader Musk-incision merger. Tesla had previously invested $2 billion in xAI before xAI was absorbed by SpaceX, leaving Tesla with an indirect stake in the new public entity.

Alphabet (GOOGL) emerged as one of the silent winners. The company holds about 4.9% of SpaceX, a stake that is now worth roughly $105 billion, one of Google's most lucrative private-market bets. Lockups and tax considerations will slow any monetization, but the paper gain is significant for a balance sheet that just absorbed a $2 trillion-valued peer.

Goldman Sachs (GS) led the deal as left bookrunner and celebrated with a building-top light display at 270 Park Avenue on Friday evening, alongside JPMorgan, which hosted roughly 250 SpaceX employees and executives Gwynne Shotwell, Jamie Dimon and others at a post-IPO reception.

Other space names sold off into the listing. CNBC noted that space stocks "deepened losses" as the SpaceX euphoria pulled capital out of the rest of the sector, a familiar pattern after mega-cap IPOs in concentrated themes.

The leveraged ETF wave: 25 funds already live

Wall Street's ETF complex did not wait for the second-day tape. SEC filings reviewed by CNBC show at least 25 exchange-traded funds tied to SpaceX were registered by the time shares began trading. More than half are leveraged or inverse products from issuers including Direxion, GraniteShares and ProShares, designed to amplify the stock's daily moves or to profit from declines.

For NQ traders this matters in two ways. First, the float available to short will be partially absorbed by these products, especially the single-stock inverse ETFs that need to borrow shares. Second, intraday volatility on SPCX is likely to be amplified by the rebalancing flow of leveraged ETFs, which mechanically buy on up days and sell on down days. Simeon Hyman of ProShares told CNBC that the combination of direct retail access, fast-track index inclusion and the leveraged product menu creates "three very powerful legs of the stool for the ecosystem to be trading very robustly."

Retail math and the small-investor squeeze

The 500-million-share day-one turnover masks an uncomfortable truth: most retail accounts did not get the allocation they wanted. The mechanics of the deal left individual investors under-water on a notional basis even after the pop. CNBC reported allocations as low as one share on some platforms, with multiple investors saying they had requested 20 to 1,000 shares. Nasdaq President Nelson Griggs told the network that roughly $15 billion of the raise came from retail investors, an unusually large slice he described as "larger than most IPOs," with the Tesla shareholder base likely amplifying demand.

The squeeze has practical consequences for the week ahead. Holders who received 10 to 20 shares at the $135 IPO price are sitting on a paper gain of $260 to $520 per position, enough to trigger profit-taking on a single bad headline. The inverse is also true: anyone who bought the open at $150 is up only modestly, and anyone who chased the $176 high is already down on a closing basis. The distribution of cost basis across the retail float will shape how SPCX trades in the absence of fresh catalysts.

What changed underneath: the AI optionality

Two structural items in the prospectus give the bull case teeth beyond Starlink cash flow. First, SpaceX retains an option to acquire the AI coding startup Cursor for $60 billion later this year, or to pay $10 billion to exit the deal, an arrangement Morningstar analyst Nicolas Owens described as an example of the company using "optionality" in its capital deployment. Cursor's market share in AI coding tools declined from 41% in June 2025 to about 26% in May, but the deal would still consolidate SpaceX's Grok models more directly against OpenAI, Anthropic and Google.

Second, SpaceX and Tesla are jointly building what the prospectus calls Macrohard, an agentic AI platform meant to emulate digital workflows across coding, product development and business processes. That positions the public SpaceX entity as a direct competitor to Microsoft's Copilot stack and Google's productivity AI, a much more ambitious framing than the rocket-and-satellite narrative implied by the ticker symbol.

For NQ traders, the takeaway is that SpaceX is not really being valued as a space company. It is being valued as a vertically integrated AI infrastructure platform with launch optionality, a comparison that puts the listing in the same conversation as Nvidia, Microsoft and the broader Nasdaq 100 leadership.

What NQ traders watch Monday

1. The SpaceX tape. Post-IPO week two is historically a difficult tape. Truist Wealth data cited by CNBC shows that 30 of the largest IPOs of the last two decades, including Alibaba, Meta and Shopify, traded lower within twelve months of debut. The sample is biased, but the warning is real. Watch for the first gap down on light volume as a signal that the easy money has been made.

2. Tesla relative strength. TSLA closed Friday with a relative weakness versus the S&P 500 and Nasdaq 100, and the relationship matters more than the absolute level. If Tesla stabilizes while SpaceX chops, capital is consolidating inside the Musk complex. If Tesla sells off further on perceived dilution or merger speculation, NQ is likely to feel the drag through the consumer-discretionary and the broader risk-on tape.

3. The leveraged ETF complex. The 25 newly registered single-stock funds will start trading on Monday and Tuesday. Expect amplified moves on SPCX, especially in the last hour of trading when leveraged products rebalance. For NQ options traders, single-stock implied volatility on the consumer-discretionary and communication-services cohorts will reprice as the new funds pull or push shares.

4. The macro tape. The SpaceX debut lands in the middle of an unusually heavy macro week. The FOMC decision on Wednesday, with new Fed Chair Kevin Warsh's first press conference, will likely set the volatility regime for the entire equity complex. Iran headlines over the weekend have already pushed oil and gold around, and a confirmed peace deal would take the geopolitical risk premium out of the tape, freeing up risk capital for high-multiple tech names. A breakdown in negotiations would do the opposite.

5. Index inclusion timing. The faster SPCX is added to major indices, the more mechanical buying hits the tape. Nasdaq said it was watching for index-eligibility decisions, and a same-week inclusion announcement is plausible given the market cap on day one. Traders should expect passive flows to add a tailwind to the listing for at least the first month.

Risks and what we do not know

Three questions remain unanswered. First, the lockup schedule: when do insiders and pre-IPO investors become free to sell, and how large are the overhangs? Second, the AI unit's actual revenue trajectory: the prospectus points to a $28.5 trillion total addressable market, but $22.7 trillion of that comes from enterprise applications where SpaceX today has "basically nonexistent" positioning, per IDC analyst Arnal Dayaratna. Third, the regulatory backdrop: Senator Elizabeth Warren, ranking member of the Senate banking committee, formally asked the SEC to delay the offering and is now pressing index providers on whether SpaceX, OpenAI and Anthropic pressured them to change listing rules. That scrutiny will not slow the stock on Monday, but it shapes the longer-term narrative for the next round of mega-cap tech IPOs.

The honest read after one session: SpaceX is a real, listed business with a real product and a real balance sheet. The valuation is a bet on a five-year AI and launch narrative that may or may not materialize. For Nasdaq traders, the work for week two is the same as it has been for the last two decades of mega-cap tech: respect the momentum, manage the position size, and remember that day-one pops and day-two performance are two different games.