Table of Contents

The US-Iran two-week truce triggered the biggest single-session oil crash since 2020, sent stocks to their best week since November, and left gold near all-time highs. Then came the inflation report.

The ceasefire that changed everything

The week opened with markets on edge. The US-Iran war, which began at the end of February, had driven crude oil from roughly $67 per barrel to as high as $117 by Tuesday April 7. The Strait of Hormuz, a chokepoint handling around 20% of the world's daily oil supply, had been effectively closed for weeks. Tankers sat anchored in the Gulf. Insurance premiums had spiked. Analysts at Goldman Sachs called it the largest supply shock in crude oil history.

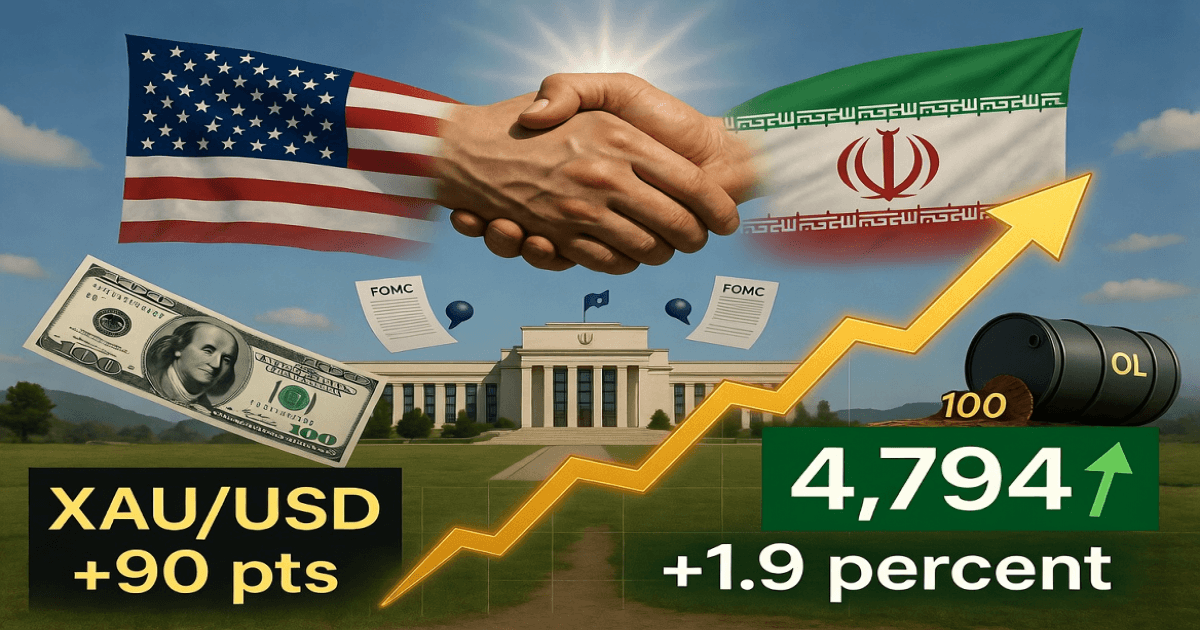

President Donald Trump had set a hard deadline for Tuesday night: open the Strait or face strikes on Iranian power plants and bridges. For most of Tuesday, markets swung with each headline. The S&P 500 at one point dropped 1.2% before recovering. Oil briefly topped $116 before pulling back as Pakistan's Prime Minister Shahbaz Sharif brokered a last-minute proposal asking Trump for a two-week extension. Less than two hours before the deadline, Trump posted on Truth Social that the US had agreed to a two-week ceasefire, conditional on Iran allowing "complete, immediate, and safe" reopening of the Strait.

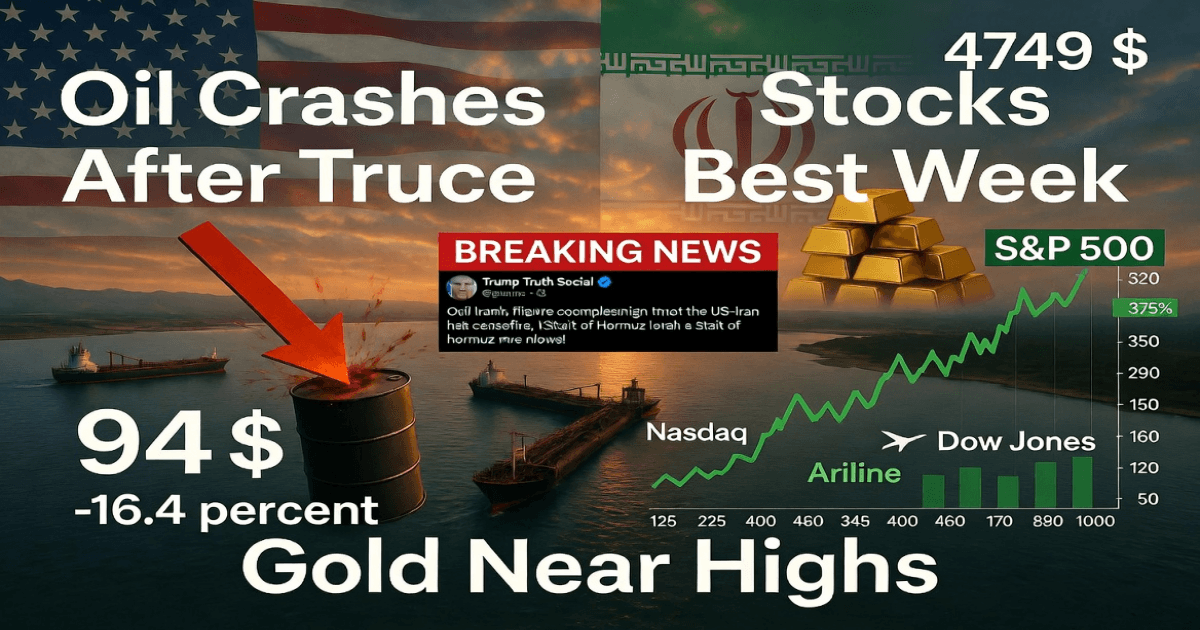

Wednesday morning was a different world. WTI crude crashed 16.4% in a single session, its largest one-day decline since April 2020, settling at $94.41 per barrel. Brent fell 13.3% to $94.75. The Dow jumped 1,325 points, its best single day since April 2025. The S&P 500 surged 2.5%, the Nasdaq added 2.8%, and European indexes followed, with Germany's DAX up nearly 5% and Korea's Kospi up 7%.

The relief was real but incomplete. Iran's Foreign Minister Seyed Abbas Araghchi said passage through the Strait would require "coordination with Iran's Armed Forces and due consideration to technical limitations." Only four ships transited the strait on Wednesday, down from 11 on Tuesday. On Thursday, Abu Dhabi National Oil Company CEO Sultan Ahmed Al Jaber posted that the strait was "not open" and that access was "being restricted, conditioned, and controlled." Oil bounced back above $99 on Thursday before settling lower again on Friday. Ultimately, WTI finished the week down 13.4%, while Brent fell about 12.7%. Both posted their worst weekly performance since April 2020.

S&P 500 and Nasdaq post best week since November

For the full week, the S&P 500 added about 3.6%, the Nasdaq Composite rose 4.7%, and the Dow gained 3%. All three indexes recorded their best weekly performance since November 2025. The ceasefire trade had a clear winner: airlines. Delta jumped 12% on Wednesday alone; Southwest surged nearly 13%, American Airlines added 11%, and the US Global Jets ETF spiked more than 11%. Energy stocks, which had been up roughly 34% year-to-date on the back of war-driven oil prices, gave back some gains as crude pulled back.

Consumer discretionary was the week's best-performing S&P 500 sector, up 2.46% on Thursday alone. Semiconductors held firm: Nvidia and Broadcom both gained on Friday and helped the Nasdaq outperform, even as the Dow slipped that day. UBS lowered its year-end S&P 500 target to 7,500 from 7,700 mid-week, citing geopolitical risk, though the firm noted that still represented a roughly 13% gain from Monday's close. Cantor Fitzgerald's chief equity strategist described the selloff in risk assets before the ceasefire as "a buying opportunity," noting that Hormuz remaining closed was still the main short-term risk.

Friday was mixed. The Dow fell 269 points or 0.56%, ending at 47,916. The S&P 500 slipped 0.11% to 6,816. The Nasdaq added 0.35% to 22,902, lifted by tech. The S&P 500 is now down less than 1% since the war began in late February.

Gold stays near $4,750 as oil crashes from record highs

Gold spent the week in a wide range, touching $4,835 at its Tuesday intraday high before pulling back when the ceasefire sparked a broader risk-on move. By Wednesday, as equities surged, gold rose to around $4,799, gaining alongside stocks rather than falling as a safe-haven trade unwound. The World Gold Council reported 21 tonnes of net inflows into global gold ETFs in just the opening days of April, which analysts described as notable for occurring during a period of declining volatility rather than during a crisis spike. Gold closed the week near $4,749, still within reach of its late-January all-time high of $5,595.

Oil's move was the headline story. Before Tuesday's ceasefire, WTI had traded as high as $117. The announcement sent it below $95 by Wednesday morning, a drop of more than $20 in hours. The price of crude on February 27, the day before the war began, was $66.96. Even after this week's crash, WTI closed Friday at $96.57, still nearly 44% above pre-war levels. Brent settled at $95.20 on Friday. Analysts at Goldman Sachs and TD Securities had previously estimated that the Hormuz blockade had removed close to 11 million barrels per day of supply from commercial stocks at its peak. Rystad Energy estimated the total cost of rebuilding energy infrastructure in the region could exceed $25 billion. The backlog of 187 tankers holding 172 million barrels inside the Gulf, tracked by Kpler, will not clear quickly regardless of how negotiations proceed.

CPI report: hot headline, cool core. The Fed can breathe

Friday's March Consumer Price Index report handed traders a mixed bag. Headline CPI rose 0.9% month-over-month, bringing the annual rate to 3.3%, the highest reading since May 2024 and a sharp jump from February's 2.4%. Almost all of the increase came from energy: gasoline prices surged 21.2% in March, the largest monthly increase recorded since 1967, accounting for nearly three-quarters of the headline print, according to the Bureau of Labor Statistics.

The more important number was core CPI, which strips out food and energy. Core rose just 0.2% for the month and 2.6% year-over-year, both one-tenth of a percentage point below consensus. Shelter prices, the biggest component of core inflation, rose 0.3% monthly, tied for its lowest reading since August 2021. The combination of a hot headline and a calm core gave the Federal Reserve analytical cover to hold rates steady and look through the energy shock. Fed funds futures markets actually raised the odds of a May cut after the release, though most economists still see the April 29 meeting as a hold.

Goldman Sachs Asset Management's global co-CIO Alexandra Wilson-Elizondo said the Fed would "look through the energy-driven noise so long as these factors hold." BMO Capital Markets warned that if the oil price shock persists, it could eventually push core prices higher. The real test will be the April CPI report, due in mid-May. If gasoline prices mean-revert as the ceasefire holds and Hormuz gradually reopens, the March spike gets treated as transitory. If oil stays elevated, the pass-through into airfares, food delivery, and transport-adjacent services could force a more hawkish reassessment. The bond market will be watching for exactly that signal.

For context: real average hourly earnings fell 0.6% in March as wages rose just 0.2% against the 0.9% CPI increase. American households with income below $30,000 could face an extra $223 annually in gasoline costs if March price levels hold. Amazon announced a 3.5% fuel and logistics surcharge on third-party sellers starting April 17. Airlines across the board raised checked baggage fees. The downstream effects of elevated energy costs are already moving through the economy.

Bank earnings, PPI data, and the fragile truce

The week ahead brings the start of big bank earnings season. Goldman Sachs reports Monday April 13, followed by JPMorgan Chase, Wells Fargo, Citigroup, Johnson & Johnson, and BlackRock on Tuesday April 14. Analysts expect forward guidance and executive commentary on the macro environment to matter more than the numbers themselves. The KBW Nasdaq Bank Index has fallen roughly 11% over the past two months as war fears and private credit concerns weighed on the sector.

March PPI data is due Tuesday and will give the second read on pipeline inflation after Friday's CPI. The Federal Reserve's Beige Book, a survey of regional economic conditions, arrives Tuesday April 15. On the geopolitical front, US-Iran peace talks are set to begin in Islamabad under Pakistan's mediation. Negotiations will center on Iran's nuclear program, the Strait of Hormuz management, sanctions, and Iran's demand for economic compensation. The two sides remain far apart. The ceasefire runs for two weeks, and markets will remain sensitive to any sign it is breaking down.