Market Sentiment

Primary Assets Affected

Table of Contents

Executive Summary

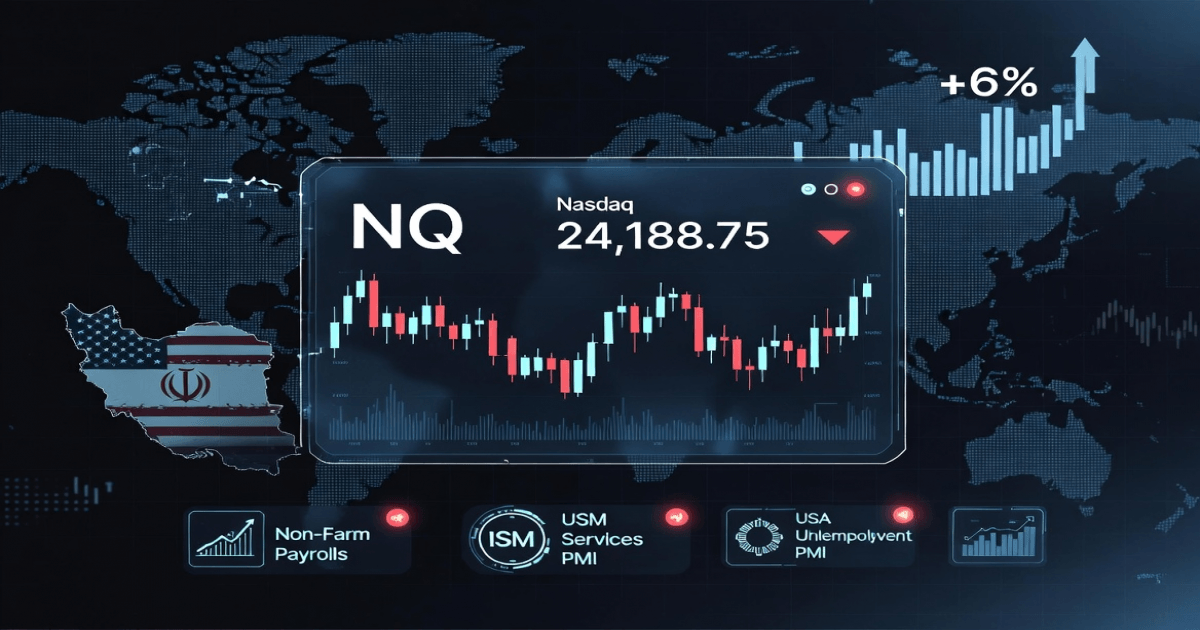

NQ is currently trading at 24,188.75, down 29.25 points on the session (‑0.12%). The intraday bias into the US session is mildly bearish to neutral as futures digest softer tech risk appetite, geopolitical tension around Iran and a heavy US data docket. Rising oil prices, stronger services PMIs and today’s US labor market releases keep macro volatility elevated and cap the upside for growth equities over the next 24 hours.

Key Market Developments (Last 24 Hours)

-

Trump signals tougher Iran strikes, hitting equity futures and boosting oil

Reuters reported that Wall Street futures slid after President Trump signaled more and tougher strikes on Iran, sending crude oil up roughly 6 percent and pressuring risk assets including Nasdaq futures. The impact on NQ is bearish as higher geopolitical risk and oil prices raise growth and margin concerns for large cap tech. -

Wall St futures slide as Iran headlines weigh on sentiment

Additional Reuters coverage highlighted renewed downside in US futures as markets reassessed the probability of further Iran escalation following Trump’s comments. This is bearish for NQ in the near term as volatility premia rise and investors trim high‑beta exposure. -

Nasdaq breadth shows stress despite recent rebounds

Recent Reuters breadth reports around the Nasdaq point to weaker underlying participation even on up days, suggesting fragility under the surface of the index rally. This is mildly bearish for NQ because narrow leadership tends to unwind faster when macro shocks hit. -

Strong US services and activity data support the “resilient growth” narrative

US ISM Services PMI printed 56.1 in March, with business activity at 59.9 and new orders at 58.6, while employment stayed above 50, confirming a solid services backdrop. This is mixed for NQ: growth support is bullish for earnings, but it reduces the urgency for Fed cuts, which is a modest headwind for duration‑sensitive tech.

Economic Calendar Highlights – Today (UTC)

| Time (UTC) | Event | Actual vs Expected (or Expected vs Previous) | Typical Impact on NQ |

|---|---|---|---|

| 12:30 | US Non‑Farm Payrolls (Mar) | 178k vs 60k expected, prior ‑133k (rev.) | Stronger jobs are usually mildly bearish (fewer Fed cuts, higher yields, pressure on long‑duration tech). |

| 12:30 | US Unemployment Rate (Mar) | 4.3% vs 4.4% expected, prior 4.4% | Slightly lower unemployment is bearish for NQ via “higher for longer” Fed expectations. |

| 12:30 | US Avg Hourly Earnings MoM (Mar) | 0.2% vs 0.3% expected, prior 0.4% | Softer wages are mildly bullish, easing wage‑inflation fears and helping valuations. |

| 12:30 | US Avg Hourly Earnings YoY (Mar) | 3.5% vs 3.7% expected, prior 3.8% | Cooling wage growth is bullish for NQ as it supports lower‑inflation narratives. |

| 14:00 | US ISM Services PMI (Mar) | 56.1 vs 54 expected, prior 55 | Strong services are mixed: bullish for earnings, bearish via higher yields and fewer cuts. |

| 14:00 | US ISM Services Prices (Mar) | 63.0 vs 70 prior | Lower prices are mildly bullish, hinting at easing services inflation. |

| 15:30 | US 3‑month and 6‑month Bill Auctions | 3‑month 3.62%, 6‑month 3.605% | Neutral to slightly bearish if higher yields persist, raising the discount rate for tech. |

| 16:35 | Fed Goolsbee speech | No data yet on tone/outcome | Could move NQ if guidance shifts on timing/size of rate cuts. |

| 19:00 | US 3‑Year Note Auction | 3.579% yield | Higher auction yields would be bearish for NQ; strong demand and lower yields would be supportive. |

Analyst Outlook & Bias (Next 24–48 Hours)

Short‑term bias for NQ into and through today’s US cash session is cautiously bearish within a broader range, with 23,800–23,900 as initial support and 24,500–24,800 as key resistance on the June contract. Strong US labor and services data confirm resilient growth and keep “higher for longer” Fed pricing in play, which, combined with Iran‑driven risk‑off and higher oil, leans against an aggressive tech rebound despite still‑solid earnings expectations.

In the next 24 hours I expect price to trade choppy between roughly 23,900 and 24,500, with sellers active on approaches toward 24,400–24,500 and dip buyers defending the 23,900–24,000 zone, where recent liquidation lows and volume congestion sit. A sustained break below 23,900 would open 23,500–23,600, while a close above 24,500 would force short covering toward 24,800, but the probability favors continued range‑bound action unless there is a surprise from Fed speakers or a material de‑escalation in Iran headlines. For intraday traders, fading extremes of this range with tight risk, while monitoring Treasury yields, crude, and any fresh geopolitical or Fed‑related tape bombs, remains the preferred approach over outright trend positioning.