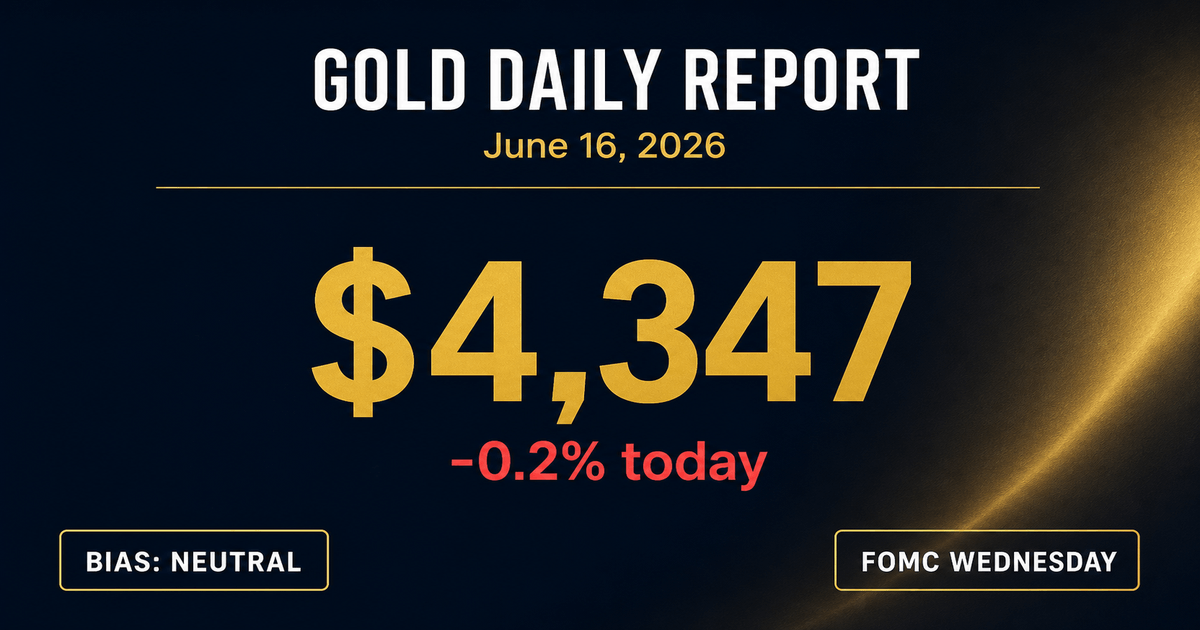

Market Sentiment

Primary Assets Affected

Table of Contents

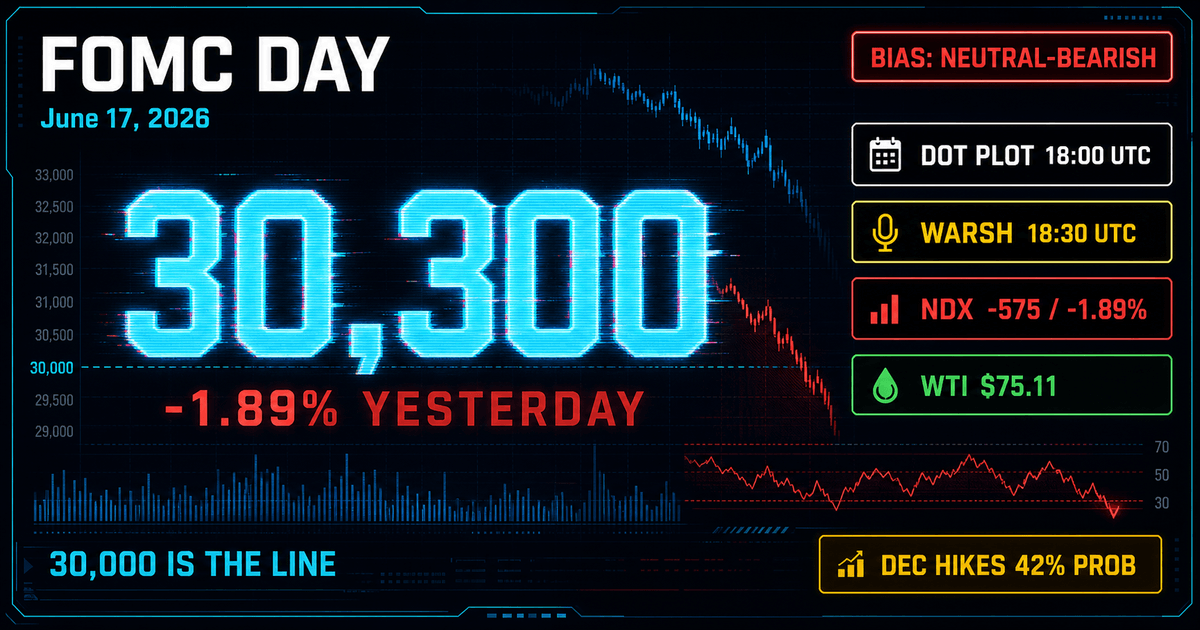

Nasdaq 100 futures are staging a tentative rebound on FOMC day, after a bruising Tuesday selloff wiped out most of Monday's SpaceX-led rally. Cross-checking three sources, the working band is 30,329 to 30,584.50 intraday (Investing.com), with futures up 0.65% pre-market (Moomoo), putting the implied open near 30,200-30,400 against Tuesday's NDX close of 29,968.13, down 1.89%. The bias is neutral with a slight bearish lean. Two-sided FOMC risk dominates, and yesterday's chip selloff reminded the buy side that the rally has been narrow and crowded.

Key Market Developments (last 24h)

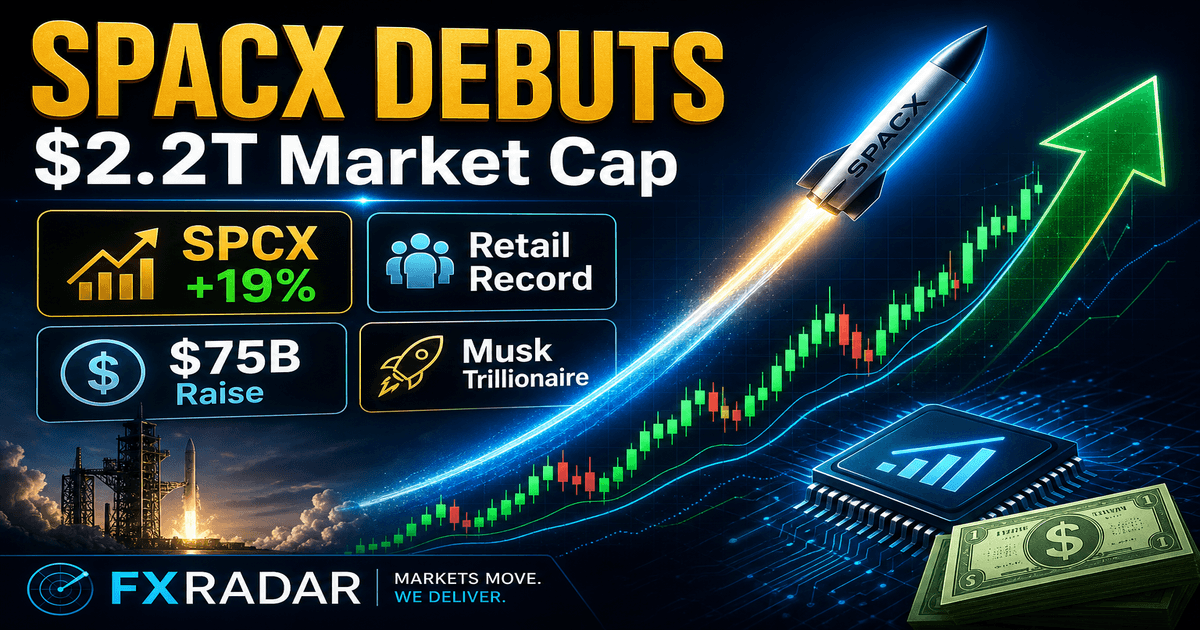

- Tuesday's chip selloff was real. NDX closed 29,968.13, down 1.89%, day range 29,962.87 to 30,560.08. Bloomberg framed it as rotation out of chipmakers after a strong advance, with SpaceX's post-IPO surge near 50% but doing little to lift the index.

- Brent crude collapsed 15% in four sessions. From above $92 to below $79, with WTI at $75.11. The Iran framework is priced as a meaningful easing of supply risk. The relief trade is already in the price.

- Pre-market bounce is fragile. Nasdaq +0.65%, S&P +0.20%, VIX 16.35. This is a re-test of the prior breakout, not a new leg up. The real test comes at 2 PM ET.

- The Fed is split. The May FOMC vote was 8 to 4, the most fractured result since 1992. Three members voted against the easing bias, one voted to cut. The policy statement is widely expected to drop the easing bias, a tightening signal even with rates unchanged.

Economic Calendar Highlights, Today (UTC)

- 13:30 UTC - U.S. Retail Sales (May). Consensus 0.3% m/m, previous 0.4%. The last data point the Fed had in hand. A hot print raises the risk of a hawkish dot plot.

- 13:30 UTC - U.S. PPI (May). Consensus 0.2% m/m, previous 0.2%. Watch core PPI for the trimmed-mean signal Warsh has flagged.

- 18:00 UTC - FOMC rate decision, statement, and SEP with dot plot. No consensus on the rate. The 2026 and 2027 medians matter more than the call.

- 18:30 UTC - Warsh press conference. The first of his career. Watch the 10-year yield in the first 30 minutes after the statement.

Analyst Outlook and Bias (next 24-48h)

Bias: Neutral with a slight bearish lean. Tuesday's selloff reset positioning, and the pre-market bounce is not strong enough to call a new uptrend. The 30,000 line on the NDX is the level that decides whether this is a healthy pullback or the start of a deeper correction. Above 30,300, the bounce can extend to 30,600 and 30,900-31,000. Below 30,000, the late-May lows at 29,800-29,900 come back into play, and a clean break opens 29,400 (20-day EMA) and 28,800-29,000.

Momentum is mixed. RSI cooled from overbought to neutral. MACD is rolling over but has not crossed bearish. The 20-day EMA at 29,400 has not been tested, which is normal in a healthy uptrend. The bigger risk is the dot plot. A hawkish surprise pushing the 2026 median dot above 3.75% would likely drive a 200-400 point drop in the NDX within 30 minutes, and the VIX at 16.35 leaves room for a spike to 20+.

FXRadar Opinion

The rate decision is not the event today. The dot plot and Warsh's first press conference are, and the asymmetry of risk is to the downside for tech. Tuesday's chip selloff was not random. The 2026 median dot is the only number that matters.

We think the Fed drops the easing bias today, that Warsh delivers a firm tone on core inflation, and that the dot plot shows zero cuts in 2026 and zero cuts in 2027. The Street is usually right on the print. We do not expect a hike path declaration, but we do expect a framework that tightens financial conditions through communication. The play is range, not trend. Above 30,300 in NQ, lean long with a stop below 30,000. Below 30,000, lean short with a target at 29,400. The rally from 28,800 to 30,900 was built on the soft-landing-plus-cuts narrative, and that narrative is breaking. For the next 48 hours, the path of least resistance is sideways to lower.