Market Sentiment

Primary Assets Affected

Table of Contents

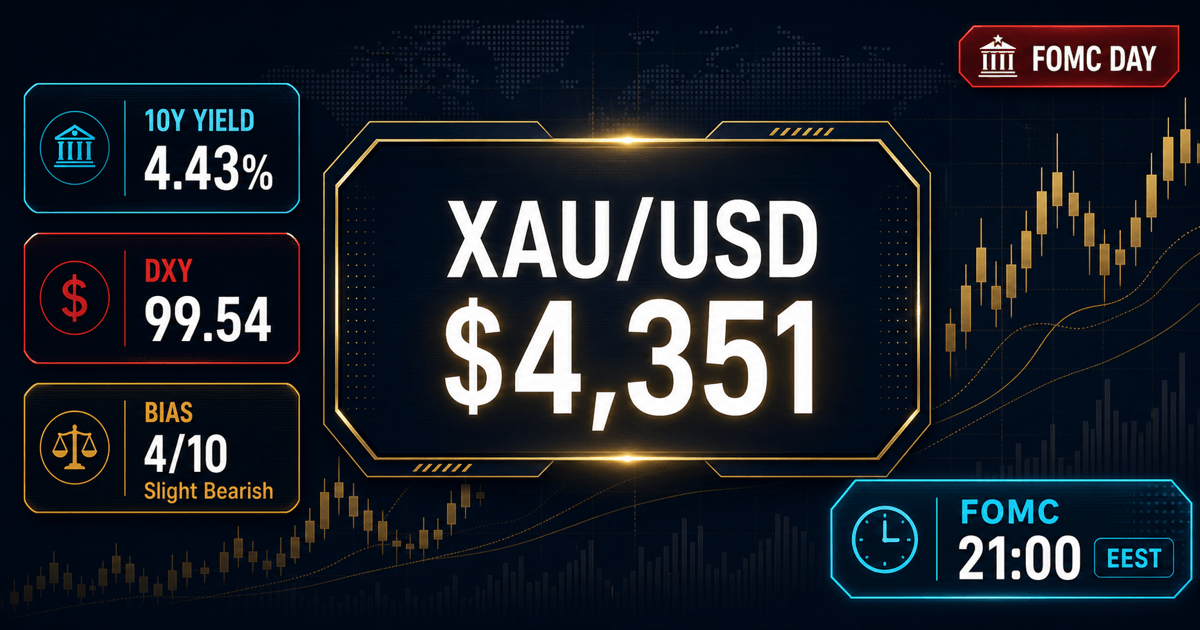

Spot gold is holding near $4,351 per ounce into the New York open, roughly flat from Monday's $4,356.74 close and stuck just under the 4,400 round. A live cross-check shows a tight band: $4,351.10 (KenMacro, Yahoo Finance 07:03 GMT), $4,330 (Facebook trader feed), and $4,350 (RoboForex morning brief). The working price is $4,345 to $4,355, with the metal consolidating in a 50-dollar range ahead of the Federal Reserve's 21:00 EEST decision. Short-term bias moves to neutral with a slight bearish lean. The 10-year real yield is back in positive territory at roughly +0.23% (4.433% nominal minus 4.2% May CPI), and the DXY has edged higher into the print. Both channels have been pulling against gold all week, and the war premium that was supposed to absorb that pressure is unwinding in real time.

Key Market Developments (last 24h)

U.S.–Iran framework deal signed, MOU slips to Friday. The White House confirmed Monday that a memorandum of understanding to end the war was signed by Trump, VP JD Vance, and the speaker of Iran's parliament. The signing ceremony has been pushed to Friday, June 19, the same day U.S. markets are closed for Juneteenth, creating a 72-hour headline-risk window over a long weekend. Fresh Israeli strikes in southern Lebanon are already complicating the diplomacy. Phillip Streible at Blue Line Futures told CNBC the "peace deal news took down Treasury yields, the dollar and oil," exactly the cross-asset path that pressures non-yielding gold.

Warsh's first FOMC opens today, and the committee is fractured. The June 16–17 meeting is Kevin Warsh's first as Fed Chair after succeeding Jerome Powell on May 22. The May FOMC vote was 8 to 4, the most divided result since 1992. December futures now price a 58% probability of a rate hike by year-end, up from roughly 40% at the start of June. Real yield is positive for the first time in weeks, the single variable with the cleanest historical correlation to gold, and the wrong color for the metal.

Economic Calendar Highlights, Today (UTC)

13:30 UTC, U.S. Retail Sales (May). Consensus 0.3% m/m, previous 0.4%. The last big consumer read before the FOMC.

13:30 UTC, U.S. PPI (May). Consensus 0.2% m/m, previous 0.2%. Watch core PPI more than the headline.

21:00 EEST / 18:00 UTC, FOMC rate decision and SEP. Hold at 3.50% to 3.75% priced at 97.4% on CME FedWatch, 99.6% on Polymarket. The dot plot is the event. Markets are watching whether the median 2026 dot moves above 3.75% to 4.00%.

21:30 EEST / 18:30 UTC, Warsh's first press conference as Chair. The market is watching whether Warsh submits his own dot. If he abstains, that itself is a signal of policy ambiguity.

Trading Levels

The current price of $4,351 sits just under the 4,400 round, the first overhead cap. Above that, $4,420 to $4,440 is the broken-range lower edge from late May, the obvious magnet on a dovish surprise. A clean daily close back above $4,440 exposes the 50-day SMA at $4,499.63 and flips the chart bullish.

On the downside, $4,345 to $4,340 is the first shelf. Below that, the 20-day EMA at $4,340.72 decides near-term direction. A sustained break opens $4,313 (Monday's low) and then $4,285, the lower boundary of the descending channel. A daily close below $4,275 puts the 2018 hawkish-hold template back on the table, with $4,100 and the 4,000 to 3,900 zone as the major downside liquidity pockets.

Momentum is tilting bearish. The 14-day RSI is in lower-neutral territory, and the MACD sits at -77.48, a clear bearish lean on the daily. Silver is outperforming gold at $70.41 (+0.73%), which historically signals positioning for a softer-dollar outcome rather than a hawkish one. That is the only counterweight on the tape.

Analyst Outlook and Bias (next 24–48h)

Bias: Neutral, with a slight bearish lean into the FOMC. The risk asymmetry has flipped from 24 hours ago. Yesterday's relief-rally bid from the U.S.–Iran framework has unwound as traders realized the real yield channel is the dominant force. A hawkish dot plot, defined as a median 2026 dot at 4.00% or above, would open the path to $4,275 and confirm the lower-high structure. A neutral-to-dovish outcome, with Warsh leaning on the oil relief to look through the May inflation spike, would pull gold back into the $4,420 to $4,440 broken-range retest. The 8–4 committee split makes both scenarios more likely than a clean consensus read.

The live war premium is the offsetting bid. Renewed Israeli strikes in southern Lebanon and the unsigned MOU keep a tail-risk floor under havens. If Warsh sounds hawkish and gold sells off into $4,275, the geopolitical channel is what would cushion the flush. A signed MOU on Friday would strip that bid and amplify any hawkish reaction.

FXRadar Opinion

The rate decision is not the event today. The dot plot is. Warsh's first press conference is. The asymmetry of risk is to the downside for gold. The move that pushed gold up 2.6% on Monday, the U.S.–Iran framework deal, was a relief rally, not a regime change. The real yield has already flipped positive, the dollar has firmed, and the metal is now stuck under the 4,400 round for the second session in a row. We think the Fed drops the easing bias today, that the median 2026 dot holds at zero cuts, and that Warsh's tone leans restrictive on inflation persistence. The Street is usually right on the print, and the print says tighter for longer. The play is range, not trend. Above $4,400, lean long with a target at $4,440 and a stop under $4,340. Below $4,340, lean short with a target at $4,275. The 4,400 to 4,340 corridor is the line that decides the next 48 hours, and the corridor is narrowing into the decision. The rally from $4,200 to $4,400 was built on the peace-deal-and-Fed-neutral narrative, and that narrative is breaking before the news even lands.